At A Glance

The recent 2021 tax plan issued by the White House calls to increase the corporate tax rate to 28 percent from the current 21 percent established in the previous administration’s 2017 tax plan. Prior to the 2017 tax rate changes the rate remained at 35%. The Internal Revenue Service publishes data on specific tax activity between 2019 and 1995. Tax data is easier to see from the recent 2017 corporate tax rate changes versus the changes from the last 25 years in 1992-1993, 1986-1988, and 1978-1979.

2017 Impacts

Between the Year 2017 and 2018 Corporate Income Taxes gross collections decreased from $338 million to $262 million, with net collections of 2018 being just over $200 million and just under $295 million in 2017. Total collections remained at $3.4 trillion the difference in corporate taxes seen aside increases in Individual, Estate and Trust Income Taxes with around $20 million from individual returns at all rates. Collections from 2019 came with net collections increasing to $225 million from $277 in gross collections.

Potential Changes

Assuming a standard increase in corporate income tax collections as has been observed historically and in consideration of an increasing GDP; the current tax rate would have generated $2 trillion over 10 years as the net corporate income taxes after refunds would have remained over $200 million each year. Net collections could be well over averages from the days of 35% if other provisions are acted effectively and successfully as well including increase enforcement from the IRS, the Global Minimum Tax, Book-Value Tax, Mergers for Foreign classification code changes, Offshore Expense Exclusions from deductible expenses and onshore expense credits.

Pandemic’s Impact

Coming out of the Pandemic, where states between California and New York had issued orders for businesses to shut down, collections could reach a new record low. 2020 saw many consumers without income, and businesses confined to online opportunities only. Despite the unemployment rate reaching 15% in the heavier part of the crisis; physical commercial activity faced absolute closure. Many businesses with multiple employees had access to paycheck protection loans, which saw companies still paying a portion of their wage expenses and retail operations expenses without income from retail sales.

2008 Financial Crisis

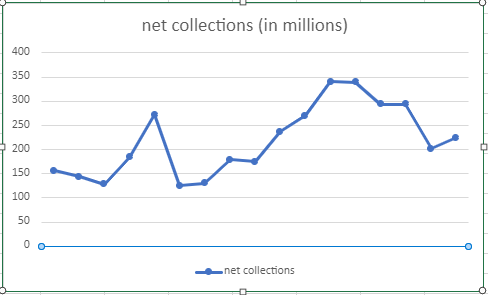

The last impact from a large economic event was the 2008 financial crisis. Gross corporate income tax collections fell more than $125 million and refunds only slightly less than $100 million, where as United States total gross collections fell $400 million. The financial services sector was impacted and all stakeholders in the economy felt an impact between workers with retirement plans, up to everyone with an investment portfolio. Net Collections from 2006 were $351 million which dropped to $130 million in 2009. Self-employment Contribution taxes remained around $53 million in the 2009 filing year. Tax collections remained low, with net 2010 corporate tax being $179 million, 2011 at $175 million, 2012 at $237 million, 2013 at $270 million. It was not until 2014 that corporate income tax rose above $300 million again with $317 million in 2014 and $340 in 2015, remaining at this increasing trend for the remaining 2 years till the 2017 tax code changes.