Want to make a personal budget, but have no idea where to start?

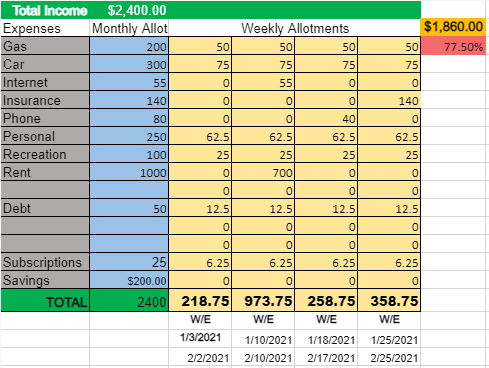

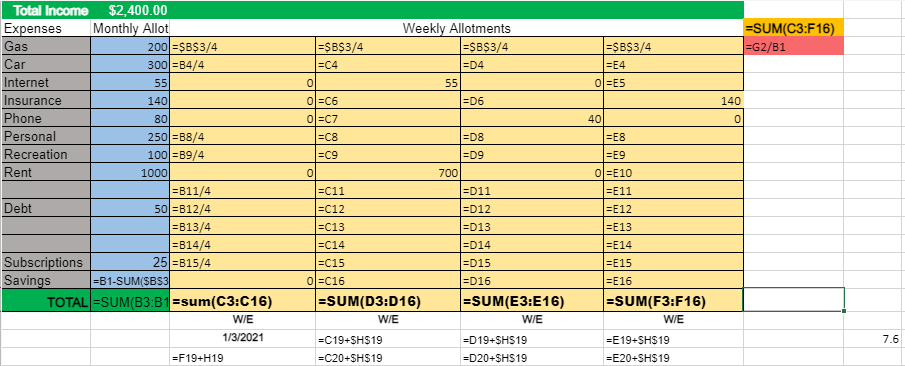

For a Simple Budget, we keep track of income and expenses. Expenses include fixed and variable costs and will have allotments set aside for those expenses.

The Two Cost Types

Fixed Costs – These are the bills that do not change, or can be expected to be the same amount for a period of time; think car payment, insurance, internet, phone, trash, mortgage or rent. These will be fixed amounts you have to pay. You can also craft your focus in your budget, whether your focus is on weekly transfer balance or monthly reducing balance amounts. A weekly transfer balance, is a balance that you update every week to pay off expenses of that week. It is beneficial for when you overspend your account runs low and with reminders enabled, you will know to slow down on the purchases. A Monthly reducing balance, means you transfer everything at once, check the balance each week and continue forward. The monthly focus can run low sooner than expected and allows over expenditure to run the whole month potentially over-budget.

Variable Costs – Are costs that will vary dependent on use or other factors. Gas for your car, electricity, water and other utilities are examples of allotments (an amount set aside that is an accurate guess of what something will cost), with an extra amount on top of estimates to cover surprises. These are the most difficult expenses to track only because they can vary, especially when your life circumstances have recently changed.

Income – All the money you bring home after taxes. To be efficient you should round down to the nearest hundred and estimate on what you will make. To be accurate, enter exact amounts.

The budget’s allotment structure will depend on each bill’s deadline. You have a monthly column to total all weekly allotments to see them compare against your income, this allows you to see your income and expenses combined result. The weekly allotment columns are where you will have to make sure you record the payments for bills on the week they occur.

Pay Periods

For example, if you are paid weekly, you could take your fixed costs and variable allotments for a whole month and divide them by 4 and there you go, you set aside the same amount every week to pay bills. If you get paid monthly it could be easier if you decide one day just for bill payments where there is enough time so that nothing is due before payment arrives. This is not the only financial control and report you can make for yourself. You should still keep records, updated check books and other important financial tools as usual.

Needed Equations

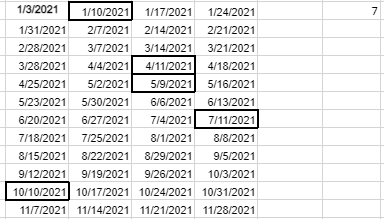

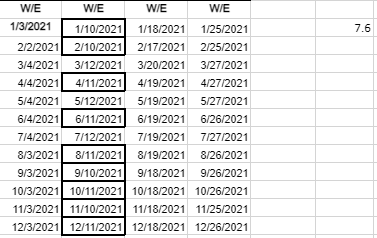

The calendar is not standardized so that each month has the same number of days. This will also make standard deviations of time not work correctly. If you took one day in the month, say the 14th, the 14th of every month will not be the same number of days between any of the other month’s 14th day. The weekly period will need to be adjusted otherwise you will eventually be early on all your bills. This is because the number of weeks and days in each month is not exactly the same, so we need to break out of differentiation. If we make every week period 7 days apart from the last, it will not be consistent, we will get ahead which is not good in this case (left photo), we need to get the Xth day of every month. If you want the budget to be within 3 days of the same Xth of every month we can use 7.6. Make sure the time you pay the bill is sooner than it is due, in case payment does not complete or any other issues that may arise.

Metric Suggestions

Daily allowance – With weekly allotments of your personal budget you can divide the amount by 7 days to figure your daily amount. This helps you when shopping for groceries, food, or services. As you shop you can keep your costs manageable and remain aware of your budget each day of the week.

Other Costs – for those times of the unexpected, it is wise to always have a little more money than you need. You never know as most of the time something can happen that draws more cost than was put aside. You would normally have to dip into your savings, but with an amount set to the side, you could be more prepared for unexpected costs. Such as memberships, car service, etc. If it is easier to just deposit it to your savings and take it out when you need it, then keep doing that.

Recreational – if you can set aside an amount for having fun, living your life with your budget in order, will feel less like a chore. Setting an amount aside for each period to have fun helps you limit how much you spend each period and leaves less up to chance. You could also plan in advance to help you know final amounts before they are spent.

Why Budget?

The problem is when people do not plan for particular spending they put themselves at risk of being behind on the ability to take control of their financial situation. Life may seem like it gets ahead of you when your finances are spent without being conscious of it in the right way, but with proper planning; you can remain in control. This Simple Account Balance Budget is a great edition to any larger consumer budget.